In the dynamic landscape of corporate compensation, companies continually seek innovative methods to attract, retain, and motivate talent. The two most popular methods in the context of a private limited company are: (i) Employee Stock Option Plan (“ESOP”); and (ii)Sweat Equity Shares.

Essentially, both the aforesaid methods give the employee a chance to own a stake in the company, which enhances the employee’s productivity at work as they inculcate a sense of belongingness to the company. However, there are significant differences between the two and we delve into the same in this blog piece.

Employee Stock Option Plan

Governing Laws: The Companies Act, 2013 (“CA 2013”) defines employee stock options (“Options”) as a right granted to an employee or director of a company to subscribe to the shares of the company at a future date at a pre-determined price.[1] The CA 2013 read with the Companies (Share Capital and Debenture) Rules, 2014 (“Share Capital and Debenture Rules”) inter alia governs the grant, issuance and transferability of Options in cases of unlisted companies.

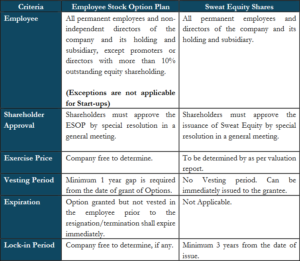

Eligibility for Options: An Option can be granted to the employees and directors of a company and its holding and subsidiary companies. The Share Capital and Debenture Rules states that an employee means a permanent employee (including those of a subsidiary or holding company) in India or abroad, and all non-independent directors.[2] Accordingly, any contractual employee or an independent director will not be eligible to receive the Options.

Further, the following persons are not eligible for receiving Options:

(a) An employee who is a promoter[3] or belongs to the promoter group; and

(b) A director who either by himself or through his relative or a body corporate, directly or indirectly holds more than 10% (ten percent) of the outstanding equity shares of the company[4].

However, registered startup companies (“Start-ups”),[5]are permitted to issue Options to the person mentioned in sub-paragraphs (a) and (b) above, up to 10 years from the date of its incorporation.

Shareholders’ Approval: A special resolution is required to be passed by the shareholders prior to the implementation of the ESOP.[6]Additional approval of shareholders by way of separate resolution is required to be obtained by the company in case of [7]:

(a) grant of Option to employees of a subsidiary or holding company; and

(b) grant of Option to identified employees, during any one year, equal to or exceeding 1% of the issued capital (excluding outstanding warrants and conversions) of the company at the time

of grant of Option.

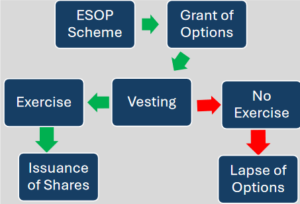

Vesting and Accelerated Vesting: The vesting period is the duration that an employee must wait before gaining the right to exercise their Options. Simply put, it is the period during which the

employee must continue to work for the company before they can purchase the shares at the predetermined exercise price. While deciding on the exercise period the organisations should be

mindful of the fact that a minimum gap of 1 (one) year has to be provided between the grant and vesting of the Options.[8] The ESOP prepared by a company may also specify the period within which Options must be exercised after an employee’s resignation which has already been vested with the employee prior to the resignation. Any Option granted but not vested in the employee prior to the resignation shall expire immediately.[9]Further, in events like the termination of an employee for cause, misconduct, insubordination, etc. the company may decide to cancel the Options vested in such employees.

In the event of the death of an employee while in employment, all Options granted shall vest in the legal heirs or nominees of the deceased employee[10]. In case an employee suffers a permanent incapacity while in employment, all Options granted as on the date of permanent incapacitation, shall vest on the employee on that day[11].

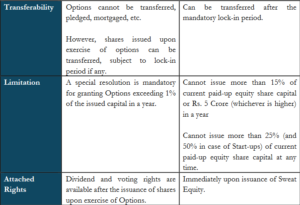

Exercise of Options: The exercise of Option refers to the process by which an employee who has been granted Options chooses to purchase company shares at a predetermined price. The exercise price for Options is determined at the time of granting the Options. This price is often set below the market price to provide a financial benefit to employees when they eventually exercise their Options. The company has the discretion to specify the exercise price Options subject to conformity with the prescribed accounting policies. The employees and the company should understand that the Options are just ‘options to purchase shares’ and prior to the ‘exercise of Options’, the employees do not get any shares in the company. Accordingly, rights attached to shares for instance dividends, voting rights, etc. are also not available prior to the exercise of Options.

Lock-in Period: The lock-in period is a specific duration during which employees, after exercising their stock Options, are restricted from selling or transferring the acquired shares. This period is designed to ensure that employees retain their shares for a set time, promoting long-term engagement with the company’s growth. However, the company has the autonomy to specify the

lock-in period for the shares issued pursuant to such Option.[12] The employee must comply with the lock-in restrictions even after resignation.

Transferability of Options: As the Options are granted to specific employees, there are restrictions on transferring the same. The Options granted to an employee cannot be transferred[13], pledged, hypothecated, mortgaged or alienated in any manner[14]. Once an Option is exercised, the shares received can be transferred, subject to the lock-in period specified under the ESOPs.

Sweat Equity Shares

Sweat Equity shares are issued by a company to its directors or employees at a discounted price or as consideration for providing services to the company like know-how or granting intellectual

property rights or value additions.[15] The expression ‘value additions’ has been defined to mean that there have to be actual or anticipated economic benefits to the company.[16] Moreover, the necessary valuation of intellectual property or such value additions is required to be carried out by a registered valuer. Such specific provisions ensure that the issuance of Sweat Equity shares at a discount or for considerations other than cash are not misused.

Governing Laws: Similar to the Options, the issuance and transferability of Sweat Equity Shares in cases of unlisted companies are governed by the CA 2013 read with the Share Capital and Debenture Rules.

Eligibility for Sweat Equity: Similar to Options, Sweat Equity can be issued to the permanent employees and directors of a company and its holding and subsidiary companies.[17] However, unlike Options, there is no restriction on the issuance of Sweat Equity to independent directors, promoters or other non-independent directors based on a shareholding threshold.

Shareholders’ Approval: A special resolution is required to be passed by the shareholders prior to the issuance of Sweat Equity. The special resolution should inter alia specify the number of shares, the current market price, consideration, if any, and the name of the employees and directors to whom the Sweat Equity is being issued.

Limit on Quantum of Sweat Equity Shares: The amount of Sweat Equity issued in a given year cannot exceed 15% (fifteen percent) of the current paid-up equity share capital or Rs. 5 (five) Crores (whichever is higher). Additionally, the total Sweat Equity issued by the company must not exceed 25% (twenty-five percent) of the company’s paid-up equity capital at any time[18].

To promote start-up culture, an exemption has been provided to Start-ups, whereby Start-ups may issue Sweat Equity not exceeding 50% (fifty percent) of its paid-up up capital upto 10 (ten) years

from the date of its incorporation or registration.

Valuation Requirements: Companies are required to obtain a valuation report from the registered valuer providing the fair price of Sweat Equity shares giving justification for such valuation.[19] Similarly, a valuation report is required to be obtained for the non-cash considerations if any, like the intellectual property, value additions or know-how being provided by the relevant employee or director[20].

Lock-in Period: The Share Capital and Debenture Rules mandate that the Sweat Equity issued shall be locked-in for a minimum of 3 (three) years from the date of allotment of shares.[21] If an employee resigns, they shall still be subject to the lock-in restrictions on transferring or selling the Sweat Equity until the completion of the aforesaid lock-in period.

As we have discussed above, both Options and Sweat Equity serve similar purposes, however, organisations should decide to implement either of them or a combination of both after giving due consideration to the steps involved and the restrictions under the law and the purpose of such incentive. For instance, a Sweat Equity does not require a waiting period whereas the Options can

be vested only after a minimum of 1 year period. Similarly, a company is free to determine the price of Options whereas a valuation report has to be obtained in the case of Sweat Equity.

Comparative Snapshot

References:

- S.2(37) Companies Act, 2013

- Rule 12, Explanation, Companies (Share Capital & Debenture) Rules, 2014

- S.2(69), Companies Act, 2013 defines a promoter to be a person names as a promoter, or who exercises control over the affairs of the company or under whose advice, directions or instructions the board of directors of the company is accustomed to act.

- Rule 12(1)(c), Companies (Share Capital & Debenture) Rules, 2014

- Start-up companies shall mean the start-ups as defined in notification number G.S.R. 127(E), dated 19th February, 2019 issued by the Department for Promotion of Industry and Internal Trade, Ministry of Commerce and Industry Government of India, Government of India.

- Rule 12(1), Companies (Share Capital & Debenture) Rules, 2014

- Rule 12(4), Companies (Share Capital & Debenture) Rules, 2014

- Rule 12(6)(a), Companies (Share Capital & Debenture) Rules, 2014

- Rule 12(8)(f), Companies (Share Capital & Debenture) Rules, 2014

- Rule 12(8)(d), Companies (Share Capital & Debenture) Rules, 2014

- Rule 12(8)(e), Companies (Share Capital & Debenture) Rules, 2014

- Rule 12(6)(b), Companies (Share Capital & Debenture) Rules, 2014

- Rule 12(8)(a), Companies (Share Capital & Debenture) Rules, 2014

- Rule 12(8)(b), Companies (Share Capital & Debenture) Rules, 2014

- S.2(88) Companies Act, 2013

- Rule 8(1)(ii) Companies (Share Capital and Debenture) Rules, 2014

- Rule 8, Explanation, Companies (Share Capital and Debenture) Rules, 2014

- Rule 8(4) Companies (Share Capital and Debenture) Rules, 2014

- Rule 8(6) Companies (Share Capital and Debenture) Rules, 2014

- Rule 8(7) Companies (Share Capital and Debenture) Rules, 2014

- Rule 8(5) Companies (Share Capital and Debenture) Rules, 2014

For any queries or discussions, you can reach out to our contributors:

Akash Kumar (akash@asqlegal.com)

Asutosh Mahapatra (asutosh@asqlegal.com)

We want to acknowledge the efforts of Ms. Shauryaa Singh, (III Year, BBA LLB, Himachal Pradesh National Law University) in assisting us with this blog piece.

Disclaimer: This work is intended for general information only and does not constitute legal or other advice and the reader acknowledges that there is no relationship (implied, legal or fiduciary) between the reader and the author/A Square Legal. It is recommended that professional advice be taken based on the specific facts and circumstances. A Square Legal neither assumes nor accepts any responsibility for any loss arising to any person acting or refraining from acting as a result of any material contained in this work.